HVAC Business Valuation: How to Value Your Company (3 Methods)

April 6, 2026 - 20 min read

April 6, 2026 - 20 min read

Table of Contents

| TL;DR Most HVAC companies sell for 2x–4x SDE (Seller’s Discretionary Earnings) for smaller businesses or 5x–10x EBITDA for larger operations. The three main valuation methods are revenue multiples (0.5x–1.5x revenue), SDE multiples, and asset-based valuation. Companies with 40%+ recurring revenue from maintenance agreements command significantly higher multiples, often 1–2 points above average. But here’s the stat that matters most: 52% of HVAC companies that go to market never sell. This guide shows you how to land on the right side of that number. |

A buddy of mine, let’s call him Rick, built a solid HVAC business over 18 years in the Atlanta suburbs. Five trucks, eight employees, $1.8 million in revenue. He was tired. Ready to sell, travel, maybe teach some trade school classes. He figured his business was worth around $1.5 million.

That was the number he had in his head for years. Round, clean, felt right.

He hired a broker, went through the process, and got a valuation back: $680,000.

Not $1.5 million. Not even close. The broker showed him why Rick was the primary salesperson, the only one who did estimates, the guy customers called directly.

He had 40 maintenance agreements on the books out of 2,000+ customers. His QuickBooks was a mess. His fleet was aging.

On paper, a buyer was purchasing a business that wouldn’t survive six months without Rick sitting in the driver’s seat.

He spent the next two years fixing everything the broker flagged. He hired a service manager, built his maintenance agreement base to 400+, cleaned up his books, and documented every process.

When he went back to market, the valuation came in at $1.35 million, and he sold within 90 days. Same business, same trucks, same zip code. But fundamentally different in the eyes of a buyer.

That’s what this guide is about. Not just the math of how to calculate a number, but the strategy behind building an HVAC business that’s actually worth what you think it is.

That’s a lot of valuation math. If you want a quick breakdown of what your HVAC company might be worth based on your revenue and service mix, let AI summarize it for you.

Get a quick valuation estimate for my HVAC BusinessKEY HIGHLIGHTS

Understanding HVAC Business Valuation

Most HVAC owners only think about valuation when they’re ready to sell. That’s a mistake. Knowing your number, even roughly, changes how you make decisions.

It tells you where you stand. Is your business an asset that’s growing in value, or a job you’ve created for yourself? A valuation forces you to answer that honestly.

It shapes strategic decisions. Should you invest $50,000 in a new truck or spend $20,000 building a maintenance agreement program? When you know what drives value, the answer becomes clear.

It protects your family. If something happens to you tomorrow, does your spouse know what the business is worth? Can they sell it? Or does the business die with you?

It gives you a timeline. If your business is currently worth $500,000 and you want to sell for $1.2 million, you now have a gap to close and a plan to build.

Every HVAC owner should know their approximate valuation and review it annually. Think of it like tracking your HVAC profit margins, you can’t improve what you don’t measure.

There are three primary ways to value an HVAC business. Each gives a different perspective, and buyers often use all three to triangulate a fair price.

This is the simplest approach. Take your annual revenue and multiply it by a factor.

Formula: Business Value = Annual Revenue × Revenue Multiple

Typical HVAC revenue multiples: 0.5x–1.5x

| Revenue Range | Typical Multiple | Example |

|---|---|---|

| Under $500K | 0.3x–0.6x | $400K revenue × 0.5x = $200K |

| $500K–$1M | 0.5x–0.8x | $800K revenue × 0.7x = $560K |

| $1M–$3M | 0.6x–1.0x | $1.5M revenue × 0.8x = $1.2M |

| $3M–$5M | 0.8x–1.2x | $4M revenue × 1.0x = $4M |

| $5M+ | 1.0x–1.5x | $8M revenue × 1.2x = $9.6M |

When to use it: Quick back-of-napkin calculation. Useful for initial conversations, but not reliable on its own because it ignores profitability entirely. A $2M company with 20% margins is worth far more than a $2M company barely breaking even.

Limitations: Revenue multiples don’t account for profitability, owner compensation, debt, or overhead. A high-revenue, low-margin company looks artificially valuable with this method.

This is the most common valuation method for HVAC businesses with revenue under $3–5 million. SDE represents the total financial benefit the owner receives from the business.

Formula: Business Value = SDE × SDE Multiple

Calculating SDE:

| Line Item | Example Amount |

|---|---|

| Net Profit (from tax return) | $120,000 |

| + Owner’s salary | $95,000 |

| + Owner’s health insurance | $18,000 |

| + Owner’s vehicle expenses | $12,000 |

| + Owner’s phone/personal expenses through business | $4,000 |

| + Depreciation & amortization | $22,000 |

| + Interest expense | $8,000 |

| + One-time/non-recurring expenses | $15,000 |

| = Total SDE | $294,000 |

SDE answers the question: “How much total money does the owner take out of this business?”

Typical HVAC SDE multiples by segment and size:

| SDE Range | Residential All-Purpose | Commercial Heating | Industrial |

|---|---|---|---|

| $500K–$1M | 5.7x | 4.8x | 5.5x |

| $1M–$5M | 6.5x | 5.4x | 5.7x |

| $5M–$10M | 7.9x | 6.4x | 7.0x |

For smaller owner-operated companies with SDE under $500K, multiples typically range from 2.75x–3.25x with a median around 2.7x.

When to use it: Any owner-operated HVAC company where the owner is actively involved. This is the method most business brokers and Main Street buyers use.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is used for larger HVAC companies, typically those with $1M+ in EBITDA or $3M+ in revenue — where the owner has stepped back from day-to-day operations and there’s a management layer in place.

Formula: Business Value = EBITDA × EBITDA Multiple

The key difference between SDE and EBITDA: SDE adds back the owner’s salary and personal expenses. EBITDA does not assume the business pays a market-rate manager to replace the owner.

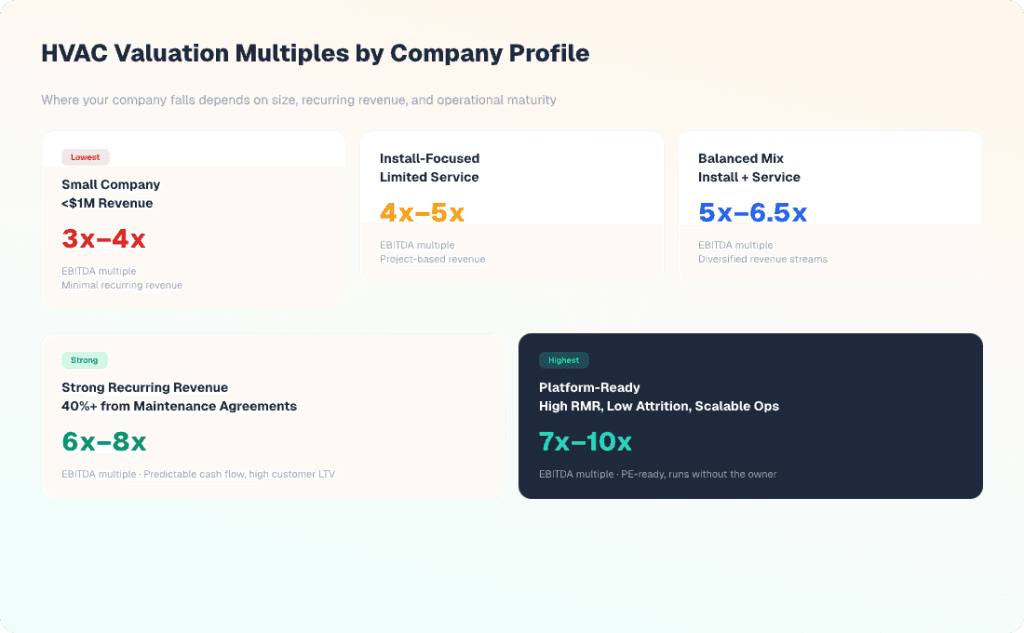

HVAC EBITDA Multiples by Company Profile:

| Company Profile | EBITDA Multiple |

|---|---|

| Small company (<$1M revenue), minimal recurring revenue | 3x–4x |

| Installation-focused, limited service base | 4x–5x |

| Balanced install/service/inspection mix | 5x–6.5x |

| Strong recurring maintenance (40%+ RMR), multi-year contracts | 6x–8x |

| Platform-ready (high RMR, low attrition, scalable ops) | 7x–10x |

EBITDA Multiples by Category and Size:

| Category | $500K–$1M EBITDA | $1–5M EBITDA | $5–10M EBITDA |

|---|---|---|---|

| Residential All-Purpose | 6.3x | 9.2x | 10.8x |

| Residential Cooling | 6.2x | 7.9x | 9.3x |

| Residential Heating | 6.1x | 8.0x | 9.6x |

| Commercial Cooling | 6.0x | 7.9x | 8.8x |

| Commercial Heating | 5.4x | 7.4x | 8.4x |

When to use it: Companies with professional management, multiple revenue streams, and enough scale that the owner’s personal involvement isn’t central to operations.

This method values the business based on its tangible assets minus liabilities.

Formula: Business Value = Total Assets – Total Liabilities

Typical HVAC assets:

| Asset Category | Example Value |

|---|---|

| Vehicles/fleet (5 trucks) | $120,000 |

| Tools & equipment | $45,000 |

| Parts inventory | $25,000 |

| Office equipment & furniture | $8,000 |

| Accounts receivable | $65,000 |

| Cash on hand | $30,000 |

| Total Tangible Assets | $293,000 |

| – Liabilities (loans, etc.) | ($85,000) |

| = Asset-Based Value | $208,000 |

When to use it: Rarely used as the primary method for profitable HVAC businesses because it ignores goodwill, the value of your customer relationships, brand reputation, and earning power. Typically used as a floor value (the minimum your business is worth) or for barely profitable companies.

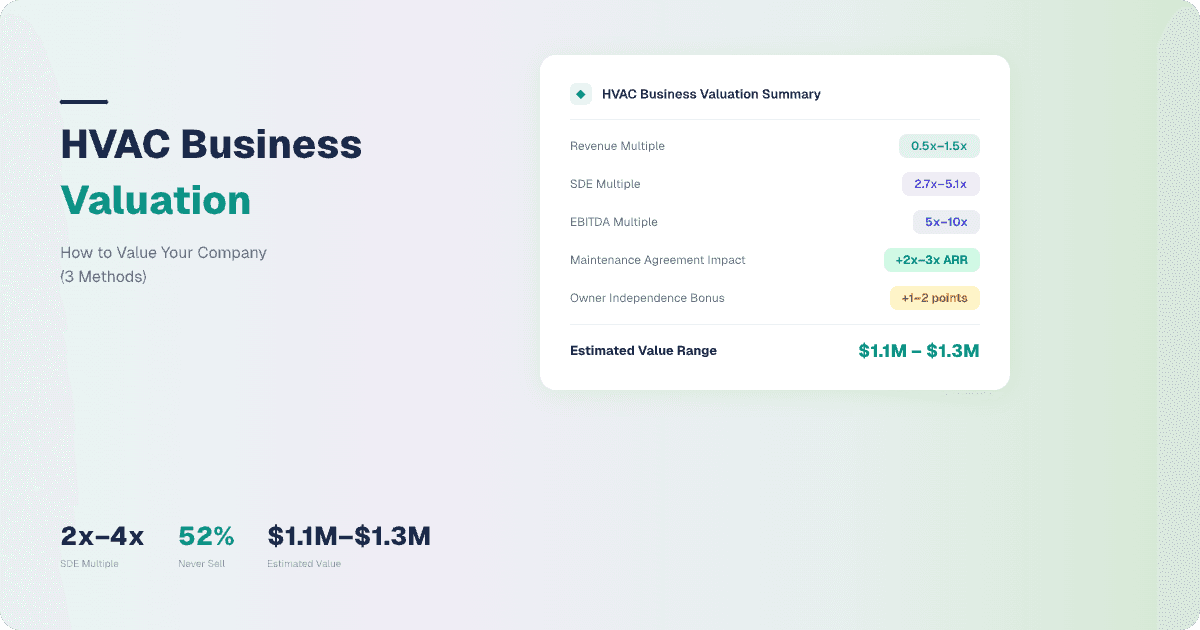

Let’s put all three methods to work on the same company. Meet “Comfort Zone HVAC” — a fictional but realistic 8-year-old company in a mid-size Southeastern market.

Company Profile:

Method 1 — Revenue Multiple:

$1,500,000 × 0.8x = $1,200,000

Method 2 — SDE:

SDE = $135,000 + $110,000 + $30,000 + $28,000 + $12,000 + $10,000 = $325,000

$325,000 × 3.5x = $1,137,500

Method 3 — Asset-Based:

Fleet ($80,000) + Tools ($35,000) + Inventory ($18,000) + AR ($55,000) + Cash ($20,000) – Liabilities ($60,000) = $148,000

Realistic Valuation Range: $1,100,000–$1,300,000

The SDE and revenue methods converge around $1.1–1.2M. The asset-based method shows a $148,000 floor, useful if the business were to close, but far below the going-concern value. A buyer would likely offer in the $1.1M–$1.3M range, with a bias toward the SDE method.

What would increase this valuation?

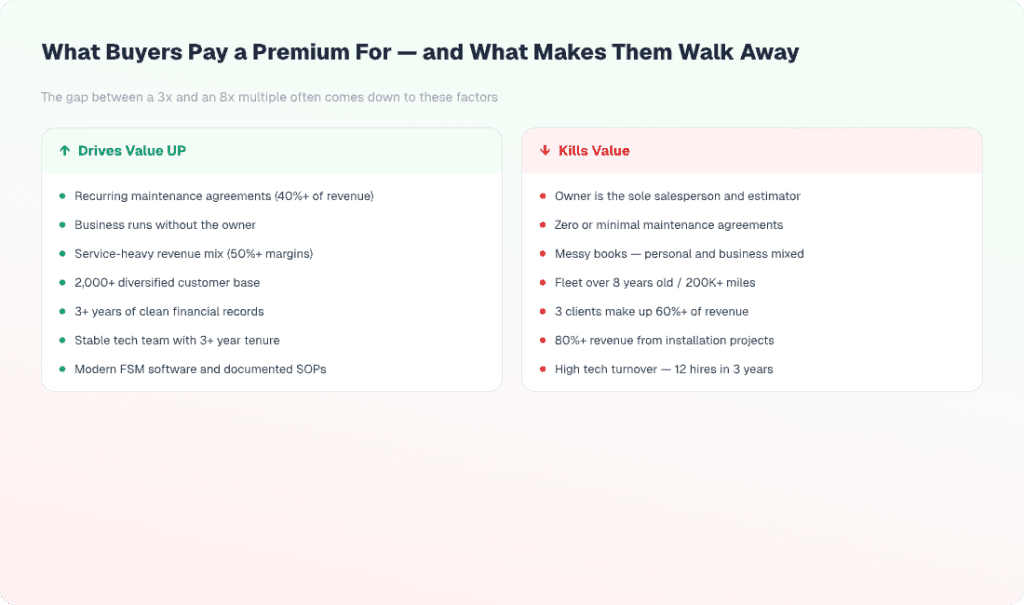

Not all revenue is created equal. Buyers pay premiums for businesses with these characteristics:

This is the #1 value driver in HVAC. A strong maintenance contract base can add 2x–3x its annual recurring value to the total purchase price.

Maintenance creates predictable cash flow, higher customer lifetime value (3–5x vs one-time service calls), and lower customer acquisition costs.

The math: 500 agreements × $250/year = $125,000 ARR. That $125,000 in maintenance revenue could add $250,000–$375,000 to your valuation, beyond what the base earnings multiple already captures.

If you don’t have a maintenance program built yet, our guide to the best HVAC apps includes the scheduling and agreement tracking tools that make running one sustainable.

A business where the owner answers every phone call, runs every estimate, and is the face of every customer relationship has a problem: the buyer isn’t purchasing a business; they’re purchasing a job. And jobs don’t sell for high multiples.

Owner independence, having a team that runs day-to-day operations without you, can add 1–2 points to your valuation. That’s potentially hundreds of thousands of dollars.

The right HVAC dispatch software is often the first system that lets owners step back from day-to-day coordination without things falling apart.

Service work generates 50–60% gross margins compared to 25–35% on installations. Buyers know this. A company with 60%+ revenue from service/repair/maintenance commands higher multiples than an install-heavy operation.

Understanding your revenue mix by job type starts with knowing how to price HVAC jobs correctly so your margins are actually as healthy as you think.

Having 2,000 residential customers is better than having 10 commercial clients who represent 80% of your revenue. Customer concentration is a risk factor that directly reduces valuation. No single customer should represent more than 5–10% of revenue.

Three years of tax returns, profit & loss statements, balance sheets, and bank statements, all consistent, all clean. If your books are in QuickBooks and your accountant can produce these in 48 hours, you’re in good shape. If your financial records are in shoeboxes and spreadsheets, you’ve got work to do.

Skilled techs with documented tenure and certifications reduce integration risk for buyers. High turnover is a red flag. A stable team with 3+ years of average tenure signals a healthy work culture, and a buyer who won’t need to rebuild the workforce after closing.

Documented processes, field service software, GPS tracking, digital job records, CRM data, these aren’t just operational improvements; they’re valuation multipliers. Buyers want to see that the business runs on systems, not tribal knowledge. The best HVAC CRM software creates exactly the kind of customer history and recurring revenue data that makes a due diligence file look bulletproof.

These are the red flags that make buyers walk away or slash their offer.

Owner Dependency: If the business can’t function for two weeks without you, it’s not a sellable business. This is the single most common valuation killer in HVAC. Buyers discount heavily for owner-dependent operations because they know revenue will drop the day you leave.

No Maintenance Agreements: A company with zero or minimal maintenance agreements is selling one-time transactions. There’s no predictable baseline revenue, no recurring customer relationships, and no built-in upsell pipeline. Buyers see this as starting from scratch every January 1.

Poor Financial Records: Mixing personal and business expenses, running cash through the business, inconsistent bookkeeping, multiple years of unfiled returns, these don’t just reduce your valuation; they kill deals entirely. Buyers can’t assess risk when they can’t see the numbers.

Aging Fleet and Equipment: A fleet of 10-year-old trucks with 200,000 miles each means the buyer needs to budget $150,000–$300,000 in vehicle replacement within 2 years. That cost comes directly out of the purchase price.

High Customer Concentration: If 3 commercial clients represent 60% of your revenue and any one of them could leave after the sale, buyers will discount aggressively — or walk away. Diversification is protection.

Installation-Heavy Revenue: Companies where 80%+ of revenue comes from installations face valuation penalties. Installation revenue is project-based, unpredictable, and lower-margin. Buyers prefer the stability of service and maintenance revenue.

High Technician Turnover: If you’ve cycled through 12 techs in 3 years, buyers see a culture problem — and a risk that the remaining team will leave post-acquisition. Retention matters.

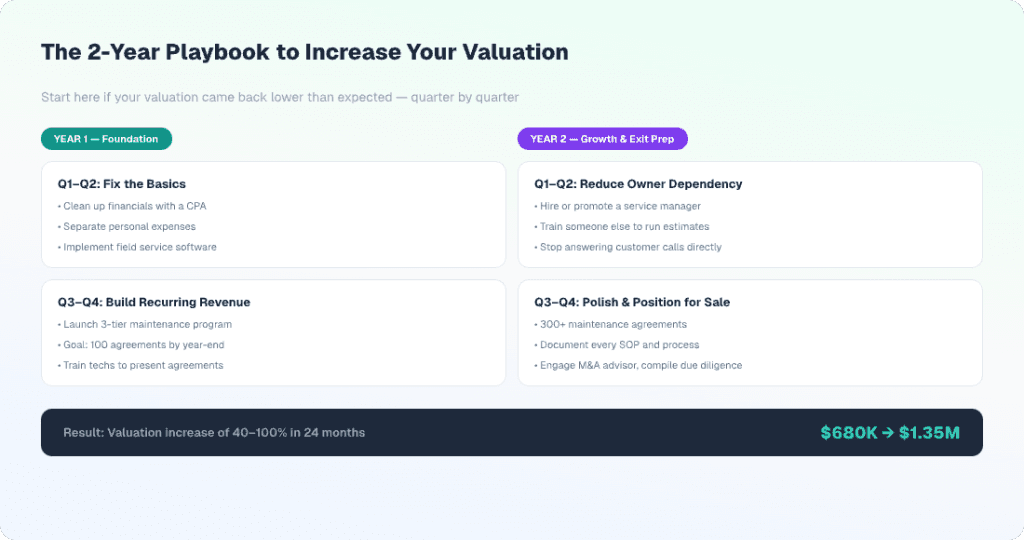

If your valuation came back lower than expected, here’s a quarter-by-quarter action plan to close the gap.

Q1–Q2: Fix the basics

Q3–Q4: Build recurring revenue

Q1–Q2: Reduce owner dependency

Q3–Q4: Scale maintenance and diversification

Q1–Q2: Optimize profitability

Q3–Q4: Prepare for market

Professional buyers, whether private equity, strategic acquirers, or individual buyers, evaluate HVAC companies through a specific lens. Here’s what they check:

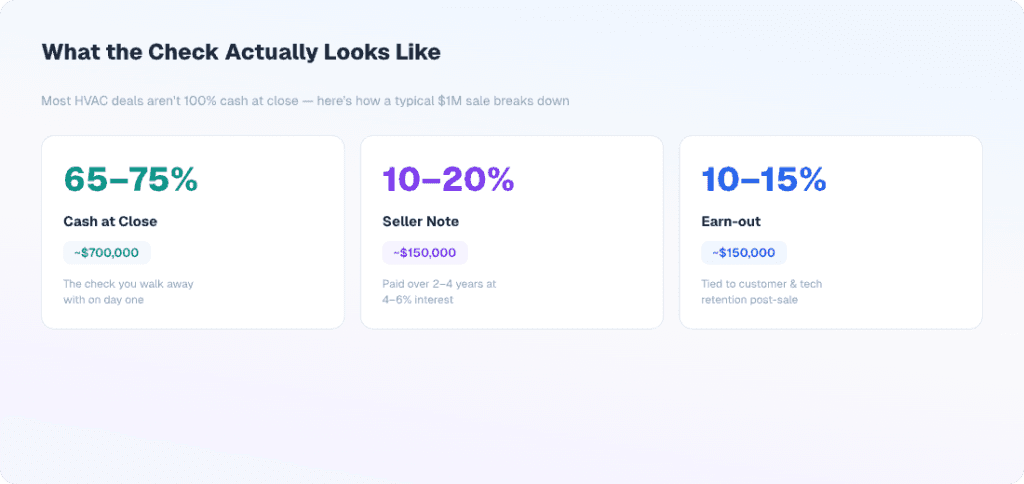

Don’t assume you’ll get 100% of the purchase price at closing. Most HVAC business sales are structured as:

| Component | Typical % | Purpose |

|---|---|---|

| Cash at closing | 65–75% | The check you walk away with on day one |

| Seller note | 10–20% | Paid over 2–4 years, typically at 4–6% interest |

| Earn-out | 10–15% | Tied to customer retention, revenue targets, or tech retention post-sale |

Example on a $1M sale:

The seller note and earn-out protect the buyer against risk, specifically the risk that customers, employees, or revenue don’t survive the ownership transition. The better your business runs without you, the more likely you’ll negotiate a higher cash-at-close percentage.

Timing matters, but less than you think. The best time to sell is when your business is ready, not when the market is theoretically optimal.

Favorable conditions:

Unfavorable conditions:

The 2-year rule: Start preparing your business for sale at least 2 years before you want to exit. The preparation itself, building maintenance agreements, reducing owner dependency, and cleaning financials, makes the business more valuable and more likely to sell. Read our guide on how to grow your HVAC business for the strategic groundwork that makes a business attractive to acquirers.

When a buyer gets serious, they’ll request a mountain of documents. Having these ready signals professionalism and speeds up the process. Deals that drag through due diligence often die.

Financial Documents:

Operational Documents:

Legal Documents:

Marketing and Brand:

Most small HVAC businesses (under $3M revenue) sell for 2.7x–3.5x SDE. A company with $300,000 in SDE would typically be valued at $810,000–$1,050,000. Larger companies with professional management and strong recurring revenue can command 5x–10x EBITDA. The exact number depends on your maintenance agreements, owner dependency, revenue mix, financial records, and team stability.

SDE (Seller’s Discretionary Earnings) adds back the owner’s total compensation — salary, benefits, personal expenses run through the business — plus depreciation, interest, and one-time costs. EBITDA does the same, except it does not add back owner compensation. SDE is used for owner-operated businesses where the buyer will replace the owner. EBITDA is used for larger companies where professional management is already in place.

Dramatically. Companies with 40%+ of revenue from service agreements command 0.5x–1.0x higher earnings multiples than installation-dependent businesses. A strong maintenance contract base can add 2–3x its annual recurring value to the total purchase price. If you have $100K in annual maintenance revenue, that alone could add $200K–$300K to your sale price.

For businesses under $1M in value, a business broker is strongly recommended; they bring buyer networks, deal structure experience, and negotiation expertise. Expect to pay 8–12% commission on the sale price. For larger deals ($2M+), consider an M&A advisor who specializes in home services or mechanical trades. They’ll charge 5–8% but often deliver significantly higher valuations through competitive bid processes.

From listing to closing, plan for 6–12 months. Well-prepared businesses with clean financials and strong fundamentals sell faster, sometimes in 90 days. Businesses with issues (owner dependency, poor records, customer concentration) can take 18+ months or never sell at all. Remember: 52% of HVAC companies that list don’t sell. Preparation is the difference.

The most common deal-killers during due diligence: financial records that don’t match what was presented, undisclosed liabilities or lawsuits, key employees threatening to leave, customer concentration higher than disclosed, and fleet/equipment in worse condition than represented. Full transparency from the start prevents these surprises.

Sell when your business is at its strongest, with growing revenue, healthy margins, a strong team, and clean books. Seasonally, listing in Q1 or Q2 allows you to show buyers a strong spring/summer season in real-time. Avoid listing when revenue is declining, key employees just quit, or you’re under personal pressure to sell quickly. The best time to start preparing is 2 years before you want to exit.